With a recession of as yet unknown severity a near certainty over the months ahead, stock market looks set to enter choppy waters. There are strong signs that the summer optimism that surrounded a rebound for major indices was premature. What was once suspected as a bear market rally now looks like an obvious one from the rearview mirror and major markets have been in steep decline as September has progressed.

The S&P 500 has lost over 8% since the beginning of the month and the Nasdaq over 5%. Even the UK’s benchmark FTSE 100 index, previously insulated from the kind of declines growth-focused Wall Street peers have suffered by its heavy weighting to commodities and energy, has fallen 4.3% in September.

Energy and commodity stocks have proven a refuge due to soaring prices resulting from Russia’s invasion of Ukraine. Financial stocks can also be expected to attract renewed interest after the Fed yesterday raised its base interest rate by 0.75% for the third month in a row. Defensive stocks like consumer staples and utilities also historically do better than cyclical sectors that rely on discretionary consumer spending during economic downturns.

But another sector might also be worth close consideration – defence stocks. Defence stocks are not, despite the association, typically defensive. Countries tend to spend more money on defence when their tax receipts are looking healthy.

But that fiscal management of national defence spending goes out the window when electorates feel threatened. And there is probably no time in modern history when developed Western economies have felt as threatened as they do right now.

Russia’s invasion of Ukraine in late February sharply focused the attention of Nato members like Germany that had for years fallen behind in their commitment to spending a minimum 2% of GDP on defence. They, and several other major Western European economies, as well as Japan, South Korea and Taiwan further east, have significantly ramped up defence spending commitments in recent months.

The huge quantities of military equipment and ammunition being supplied to Ukraine’s armed forces, and rapidly spent keeping Russia’s invading forces from making further gains and recently counter-attacking, also needs to be replaced. Much more will also have to be delivered to Ukraine before there is any realistic hope of Russia being defeated, an outcome the West has heavily committed to supporting.

With Putin’s sabre rattling and nuclear threats this week also being interpreted as a new escalation in his proxy confrontation with the West, there is unlikely to be any imminent let up in renewed defence spending. If anything it is likely to increase and an economic recession as a backdrop will not, under the circumstances, prove a deterrent.

Defence stocks have been one of the few sectors to do well this year but they could still do much better if elevated military spending continues, as it seems certain to. That will draw the attention of investors with a strong incentive to put their money into countercyclical sectors over the near term at least, further boosting valuations.

If you do consider investing in defence stocks as a potential growth sector amid a broader bear market, which UK-based companies are worth your appraisal?

Source: Investors’ Chronicle

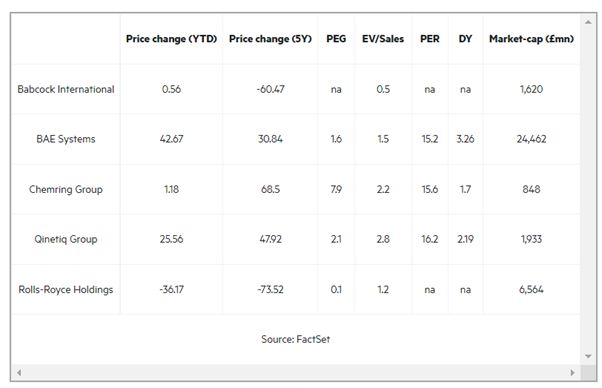

QinetiQ

Defence technology company QinetiQ had seen its valuation drop by around 17% from early August until this week but has been boosted again by Putin’s threats to resort to nuclear weapons.

It is estimated the UK could increase its service personnel count by 27%, as many as 42,000 new recruits, over the next few years. All of those troops will require the specialist training Britain’s armed forces are renowned for. That’s something QinetiQ, spun out from the UK government’s Defence Evaluation and Research Agency, is likely to benefit from as a provider of training and mission rehearsal systems.

BAE Systems

BAE Systems, the defence and aerospace company, has seen its market capitalisation gain almost 46% this year and has held steady over the past few months while others in the sector have seen their valuations dip. If defence spending remains elevated or even increases from current levels, BAE will be in a very strong position to benefit.

The company is the UK’s largest defence group and generates the majority of its revenue from fighter jet programmes—especially the F-35 Lightning and the Eurofighter Typhoon. BAE’s customers include governments in the US, UK, Australia and Saudi Arabia.

Rolls-Royce Group

Unlike the other stocks mentioned here, Rolls-Royce is not a pure defence play with the majority of the company’s revenue coming from civil aerospace contracts providing and maintaining jet engines for civil airlines. However, its valuation is particularly low at the moment as a result of the impact of the Covid-19 pandemic leaving the potential for plenty of upside.

A recession would not be good for civil aviation but it can’t get much worse than the past couple of years. The group could also be significantly boosted by defence contracts with Rolls-Royce engines also used in military aircraft, transport vehicles and naval vessels.

Babcock International

It’s been a volatile year for Babcock, which is also heavily exposed to the civil nuclear power sector as a specialist in the construction and decommissioning of nuclear power plants. But nuclear power has a bright future and Babcock also specialises in nuclear submarine construction and decommissioning.

The company also offers fleet management services for military vehicles and provides technical training and maintenance support for military infrastructure. It has a well-diversified client base with customers in the UK, Europe, Africa, North America and Australia.

Chemring Group

Chemring Group’s share price is up 63% in the last 5 years, clearly ahead of the market. However, despite the rise in military spending this year more recent returns haven’t been as impressive and investors are disappointed by dividend growth.

Chemring has moved into profitability from losses over the past few years and dividends have been steadily growing, even if shareholders would like more. The company provides chaff for aircraft and makes sensors used in electronic warfare, explosive hazard detection and chemical and biological detection. It also develops and manufactures advanced expendable countermeasures and countermeasure suites for protecting air, sea and land platforms against the threat of guided missiles.

Higher international defence spending and a continuation of the war in Ukraine will see robust demand for all of those products and services.